When people hear the term “liens explained,” they often assume it’s a complicated legal concept reserved for lawyers, banks, or courts. In reality, liens are a fundamental part of everyday financial life. If you’ve ever financed a car, taken out a mortgage, or hired a contractor, you’ve likely encountered a lien — whether you realized it or not.

In this in-depth guide on liens explained, we’ll break down what liens are, how they work, the different types of liens, and what they mean for property owners and creditors. I’ll keep it casual, but you’ll walk away with expert-level clarity. Let’s dive in.

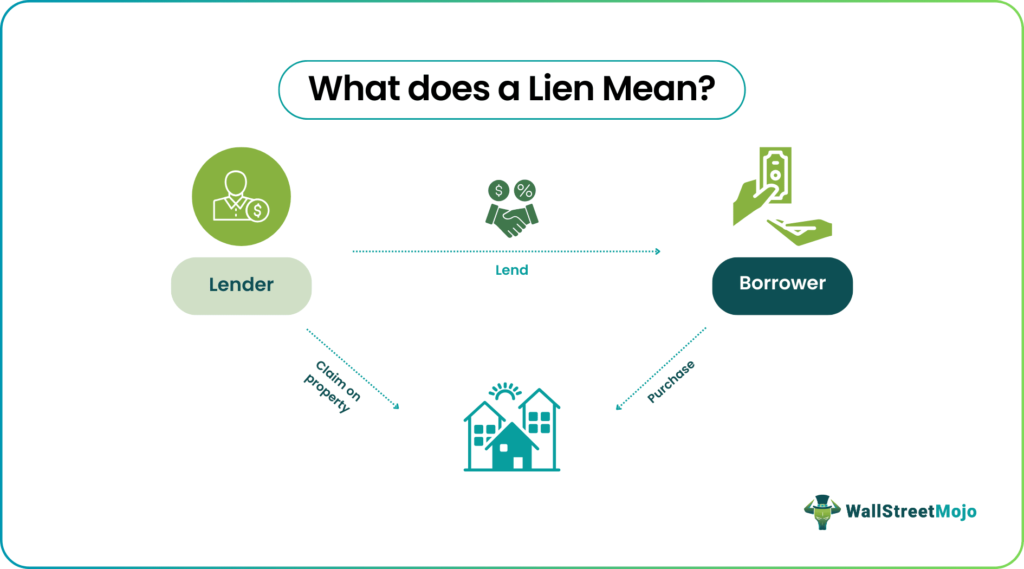

What Is a Lien? (Liens Explained in Simple Terms)

At its core, a lien is a legal claim against a person’s property. That’s it. When discussing liens explained, the simplest definition is this: a lien gives someone the right to keep or sell your property if you fail to pay a debt.

Think of a Liens Explained as a form of security. When a lender gives you money — for example, to buy a house — they want protection. So they place a lien on the property. If you don’t repay the loan, they can legally seize or force the sale of that property to recover what they’re owed.

Liens can apply to many types of property. Real estate is the most common example, but vehicles, equipment, bank accounts, and even personal property can have liens attached. In the world of finance and law, understanding liens explained properly means understanding that a lien does not necessarily mean someone owns your property — it means they have a claim against it.

Another key point in liens explained is that liens affect your ability to sell or refinance property. If you try to sell a house with a lien on it, the lien must usually be satisfied (paid off) before ownership transfers to the buyer. That’s why liens are taken very seriously in real estate transactions.

How Do Liens Explained Work?

To fully understand liens explained, you need to understand how they function in practice. A lien typically arises when a debtor fails to meet a financial obligation. However, some liens are voluntary, while others are imposed by law.

A voluntary Liens Explained happens when you agree to it. A mortgage is the perfect example. You sign loan documents that clearly state the lender will place a lien on your property until the debt is repaid. In this case, both parties knowingly accept the arrangement.

Involuntary liens, on the other hand, are imposed without your consent. For example, if you fail to pay taxes, the government can place a tax lien on your property. If you lose a lawsuit and don’t pay the judgment, the court may authorize a judgment lien. In these cases, liens explained becomes especially important because many people are unaware they even have a lien until it affects their credit or property sale.

Once a lien is in place, it establishes priority. This means if the property is sold, creditors are paid in a specific order. Usually, the first lien recorded has the highest priority. This concept is crucial in liens explained, especially in foreclosure situations where multiple creditors may be involved.

Types of Liens You Should Know

When people search for liens explained, they often want to understand the different categories. Not all liens are the same, and each type serves a specific purpose.

1. Mortgage Liens

Mortgage liens are the most common type. When you borrow money to purchase a home, the lender places a mortgage lien on the property. If you default, the lender can foreclose. In discussions about liens explained, mortgage liens are often the starting point because they’re so common.

2. Tax Liens

If you fail to pay property taxes or income taxes, the government can impose a tax lien. Tax liens are powerful because they often take priority over other liens. In the hierarchy of liens explained, tax liens are among the most serious due to the authority behind them.

3. Mechanic’s Liens

Contractors and construction companies use mechanic’s liens when they are not paid for work performed on a property. If a homeowner refuses to pay for renovations, the contractor can file a lien against the property. This ensures payment if the property is sold. Mechanic’s liens are frequently discussed in liens explained within the construction industry.

4. Judgment Liens

When a court rules that you owe someone money and you fail to pay, the creditor can obtain a judgment lien. This lien attaches to your property and can complicate any future sale. In many real-world cases of liens explained, judgment liens surprise property owners the most.

Each type of lien operates under specific legal rules, but they all share the same underlying principle: securing repayment of a debt.

What Happens If You Have a Lien on Your Property?

A common concern when researching liens explained is whether having a lien means losing your property immediately. The answer is no — not necessarily.

A Liens Explained does not automatically result in foreclosure or seizure. Instead, it gives the creditor a legal right to pursue those actions if the debt remains unpaid. Many liens remain in place quietly while payments continue as agreed.

However, liens can create serious obstacles. For example, you cannot transfer clear ownership of property without resolving any existing liens. If you attempt to sell a house with an unpaid lien, the debt typically must be satisfied at closing. In that sense, liens explained also involves understanding how liens restrict financial flexibility.

Liens can also impact your credit score. Tax Liens Explained and judgment liens, in particular, may appear on public records and negatively affect your financial profile. That’s why resolving liens promptly is always advisable.

How to Remove or Satisfy a Lien

One of the most practical aspects of liens explained is understanding how to remove them. In most cases, the solution is straightforward: pay the debt.

When the underlying obligation is satisfied, the creditor issues a Liens Explained release. This document officially removes the lien from the public record. In real estate transactions, this process is critical because buyers require proof that the title is clear.

Sometimes, disputes arise. For example, a contractor may file a mechanic’s lien even if the homeowner believes payment was made. In such cases, legal action may be necessary to resolve the disagreement. Understanding liens explained includes recognizing that liens can sometimes be filed improperly or fraudulently.

In rare situations, liens may expire after a certain statutory period if the creditor does not enforce them. However, relying on expiration is risky. The safest approach is always to resolve the underlying debt or challenge the lien legally.

Why Understanding Liens Is So Important

The reason liens explained is such an important topic is simple: liens affect ownership rights. Property ownership is not always absolute. When a lien exists, your rights are partially shared with a creditor.

For homeowners, liens directly impact the ability to refinance or sell property. For business owners, liens on equipment or assets can disrupt operations and financing opportunities. For investors, liens can represent either risk or opportunity, depending on the context.

Financial literacy includes understanding how secured debt works. In that framework, liens explained becomes essential knowledge. Without understanding liens, individuals may unknowingly jeopardize their property or underestimate financial risks.

Moreover, Liens Explained play a central role in credit markets. Lenders are willing to provide large sums of money because liens reduce their risk. So while liens can feel restrictive, they are also a foundational mechanism that makes modern lending possible.

Final Thoughts: Liens Explained Clearly and Simply

By now, you should have a solid grasp of liens explained from both a practical and legal perspective. A lien is simply a legal claim against property used to secure payment of a debt. It can be voluntary or involuntary, common or complex, temporary or long-term.

Understanding liens explained helps you navigate mortgages, taxes, contractor agreements, lawsuits, and financial planning with confidence. Instead of viewing liens as mysterious legal threats, you can see them for what they are: tools designed to protect creditors while shaping how property ownership works.

If you remember one key takeaway from this guide on liens explained, let it be this — a lien does not mean you lose ownership immediately, but it does mean someone else has a legal interest in your property until a debt is resolved.